The recent policies of the government affecting the pulses sector are betraying New Delhi’s chaotic thinking and knee-jerk reaction. First, as part of the agricultural market reform package, the government placed lentils outside the ambit of the law to intimidate other essential commodities such as oilseeds.

The move sought to justify the removal of stock restrictions and other restrictions that would improve the marketing of the crop so that growers, exporters, and others could confidently generate sufficient inventory.

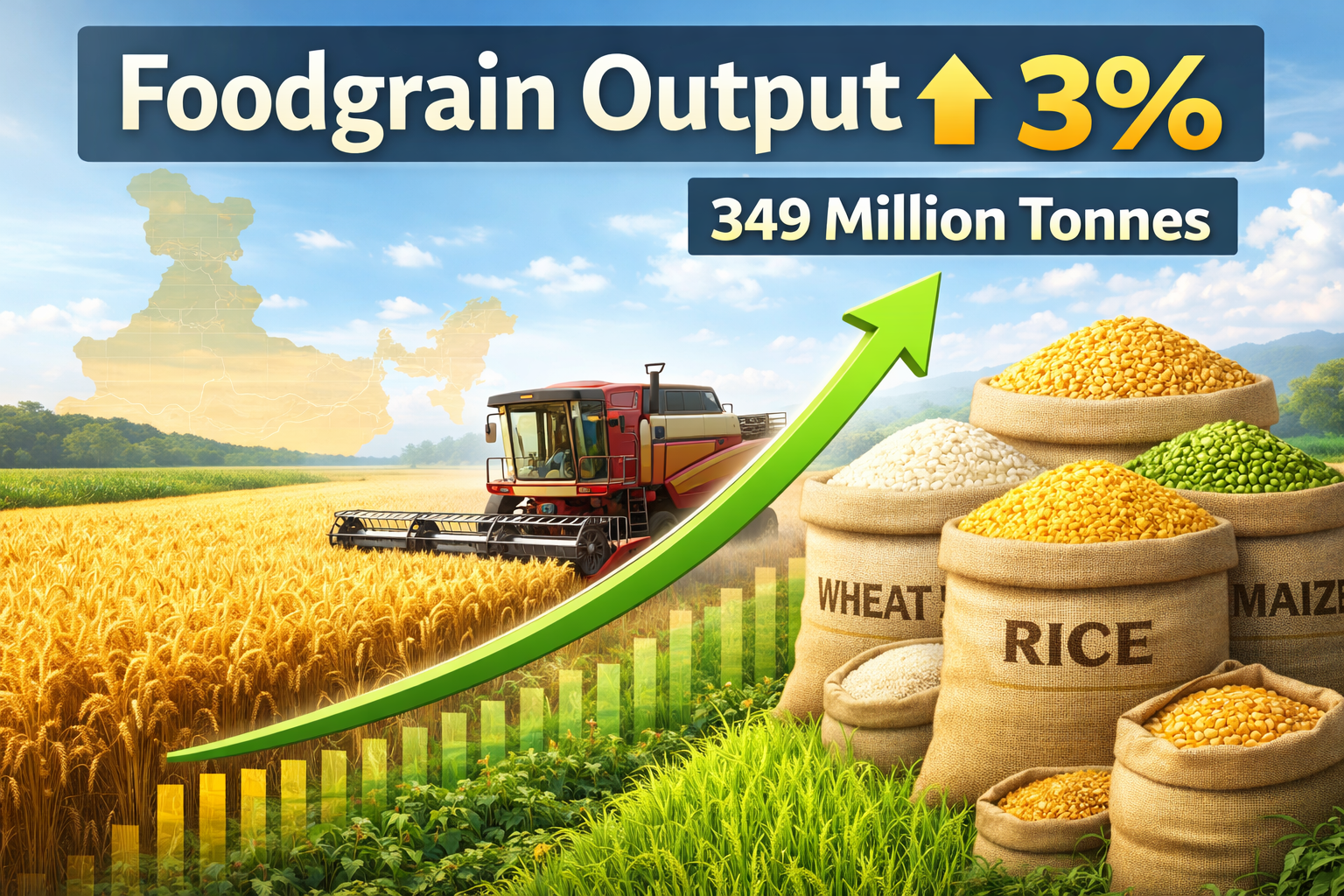

The Ministry of Agriculture’s third estimate released on May 25 recorded lentil production for 2020-21 at 25.6 million tonnes (23.0 million tonnes in the previous year), although private estimates were at least 10% lower. Despite the fact that the prices of registered-produced pulses have risen above the minimum support price (MSP) in March-April, food inflation, driven by rising crude and cooking oil prices in the international market, will continue to rise.

The ultimate arbiter of market supply-demand fundamentals is the threat, but the government has refused to see the reality. Production numbers were called into question as panic set in.

On May 14, millers, importers, and shareholders were asked to declare shares on a real-time basis. While the stock announcement may seem harmless in its face, it upset frightened traders. Despite the release of the import quota for the fiscal year 2021-22, dur / arhar (pigeon pea), yurt (black matte), and moong (green gram) are set to be free to import until October 31st. Under the conditions then obtained, import liberalization was a welcome decision.

Meanwhile, the market began to cool; But the worst has not yet come. On July 2, the government issued an ECA to re-impose specific stock limits on wholesalers, retailers, millers, and pulses importers. It seeks to justify this by claiming that it is part of the government’s ongoing effort to reduce the prices of essential commodities such as pulses.

As a result, repression is not on prices, but on pulse sector shareholders, including farmers, millers, and traders. The new Climptown ECA completely rejects the justification given when it was diluted. While extraordinary circumstances demand extraordinary policy responses, there is nothing to say that pulses will contribute to runaway inflation.

Pulse traders are tense today. They have not forgotten the hardships they experienced during the 2015-2016 period by indiscriminate trials and confiscation of shares. It is important for policymakers to recognize the vital role of the supply chain in ensuring that essential foods are distributed throughout the length and breadth of the country throughout the year.

The government’s turn-failure shows it in a bad light. Lack of business intelligence and market overview. There is little clue in New Delhi about the exact crop size, demand, import requirements, actual import, and price outlook. Partner advice is the way forward. Importers and traders who are to be treated with respect are not to be regarded as enemies of the state.